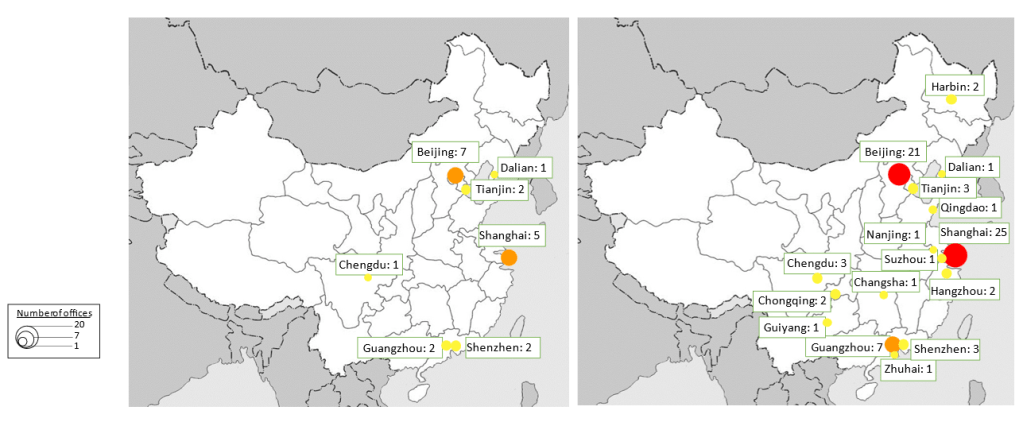

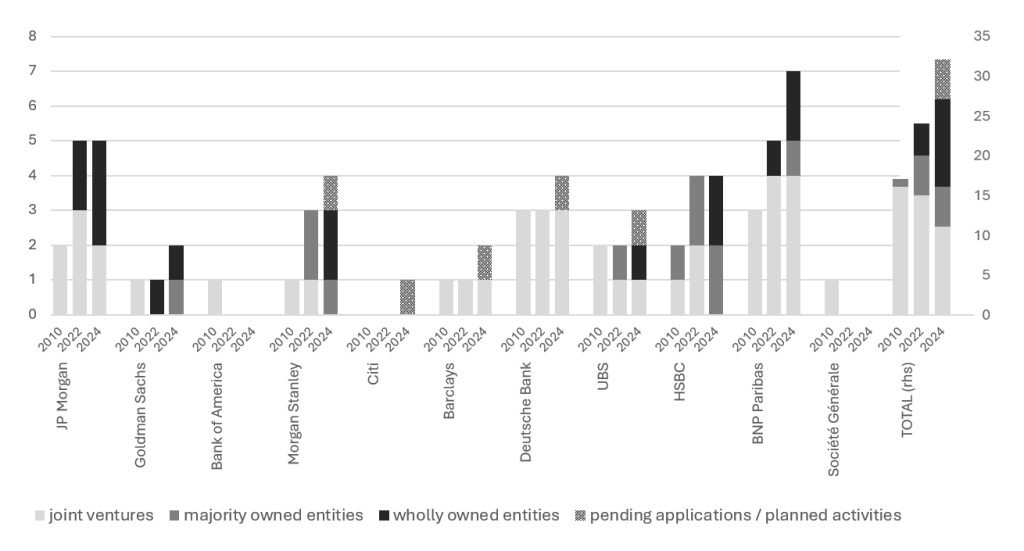

In the last decades, private global financial firms – or Wall Street – have greatly expanded their China engagement. From investment banks, to asset managers or hedge funds, Wall Street firms have ramped up their China business activities by creating subsidiaries, obtaining licenses and participating in Chinese capital markets. While US portfolio investment into China amounted to only USD50 billion in 2003, by 2020 it had surged to USD1.4 trillion—making China the 3rd largest destination for US investors globally.

This financial integration takes place within the context of a global financial system based on liberal norms of open, lightly-regulated, internationally-integrated financial markets and centered around an Anglo-American core that reproduces US power (Drezner and McNamara, 2013). Importantly, these ideas and power constellations that underpin the global financial system are largely implemented and reinforced by private actors (Sinclair, 2005, Porter, 2011). Within International Political Economy (IPE) literature, Wall Street is thus often depicted as paragons of liberal capitalism (Harmes, 1998, Gabor, 2021). However, China is characterized by a fundamentally different state-market configuration (Naughton and Tsai, 2015). Since the re-opening of Chinese finance in the 1990s, a different way of thinking about, managing and governing financial markets has consequently emerged (Gruin, 2019). Influenced by China’s state-capitalist economic system, state control and national development are the underlying principles that govern these markets (Petry, 2020a). At the same time, my preliminary research indicates that Wall Street played a crucial role in helping to develop China’s financial system.

Given these two different ways of organizing capital markets, this project investigates how Wall Street’s relationship with China has evolved over the last decades. Which role did Wall Street play in the growth of Chinese capital markets? Has China adopted liberal norms of market organization and accepted incumbent power constellations? Or has Wall Street accepted China’s non-liberal norms of operating markets? And if so, what are the consequences for US financial power?

The aim of this project is thus to investigate Wall Street in China, its role in China’s financial development and implications for the global financial system. Based on preliminary research, my working hypothesis is that Wall Street has largely supported China’s alternative model of market organization – financially through increasing investments, instructively through transferring knowledge, and normatively through legitimizing its non-liberal market practices. The project thus develops the concept of the malleability of global finance – rather than a paragon of liberal capitalism, Wall Street has accommodated Chinese finance, compromising liberal norms and US power – even amidst growing geopolitical tensions – resulting in a reconfiguration of global financial governance.

___________________

major publications

Petry, J. (2025). Wall Street in China: the malleability of global finance in the age of geopolitics. Review of International Political Economy, 32(4), 970–1001.

___________________

data insights

____________

____________

____________